Carlos Scarpero- Mortgage Broker

How To Use A VA Bonus Entitlement Calculator

Table of Contents

- Key Takeaways

- Why Bonus Entitlement Matters When You Have Multiple VA Loans

- Gather What You Need: Your Certificate of Eligibility and Property Info

- Using the VA Bonus Entitlement Calculator Step-by-Step

- Important Details to Keep in Mind

- Why Use an Online Calculator? Because It’s Easy and Accurate!

- FAQs About VA Bonus Entitlement and the Calculator

- Final Thoughts

Key Takeaways

- Bonus entitlement is crucial if you have multiple VA loans at the same time, allowing you to understand how much home you can buy with zero down.

- You’ll need your Certificate of Eligibility (COE), the loan limits for your area, and details about your current VA loan to calculate remaining entitlement.

- Using an online VA bonus entitlement calculator simplifies figuring out whether you owe a down payment or can buy with zero down.

- Loan limits vary by county and property type, so knowing these details is essential for accurate calculations.

- If you’re maxed out on entitlement, you may have to make a down payment, even if you qualify for the loan otherwise.

- My free online calculator helps you quickly determine your remaining entitlement and down payment requirements.

Why Bonus Entitlement Matters When You Have Multiple VA Loans

First off, let’s talk about why bonus entitlement is important. If you’re in the position of having multiple VA loans simultaneously—maybe you’re relocating for a PCS move or simply want to keep your current home while buying another—you need to understand your remaining entitlement. This is the amount of VA-backed loan benefit you have left to use without having to put money down.

Even if you qualify for both loans based on income and credit, the VA entitlement piece determines if you might owe a down payment on the new home. Why? Because VA loans don’t have a fixed dollar limit. Instead, your entitlement limits how much the VA will guarantee. If you’re “maxed out” on your entitlement, you’ll have to bring some cash to the table.

Just a quick heads-up: there’s a minimum loan size to consider, which is $144,000. While it’s rare to encounter this nowadays, especially in places like Ohio where I’m based, it’s still something to keep in mind when planning your next purchase.

Gather What You Need: Your Certificate of Eligibility and Property Info

Before diving into calculations, you’ll want to have a few things ready:

- Your Certificate of Eligibility (COE): This document shows your current VA loan usage, including any active loans and the entitlement charge against them.

- The location of the property you’re considering: Specifically, the state and county because loan limits vary by county.

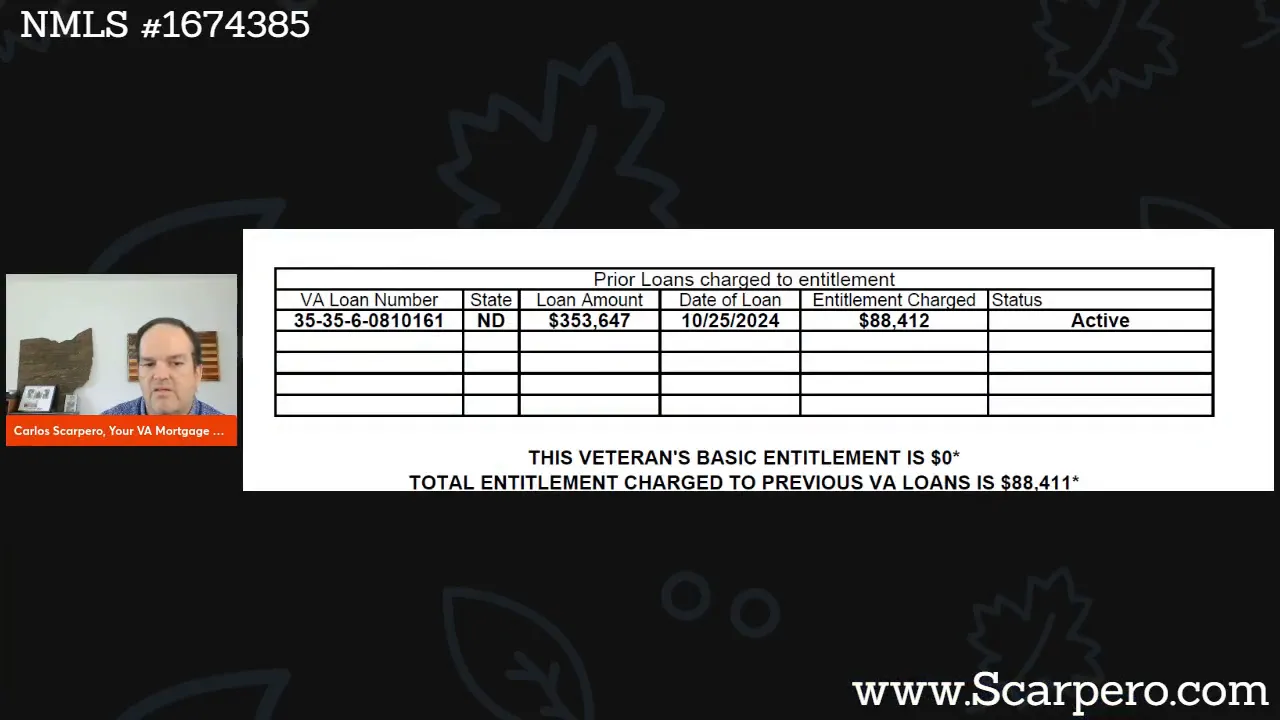

Your COE is essentially your VA loan “scorecard.” It lists your active loans, the amount of entitlement used, and other key info. For example, you might see something like this:

On this COE, you can find the “entitlement charge” number, which represents how much of your entitlement is currently tied up in an active loan. In my example, it’s $88,412. This is the key number you’ll plug into the calculator.

Using the VA Bonus Entitlement Calculator Step-by-Step

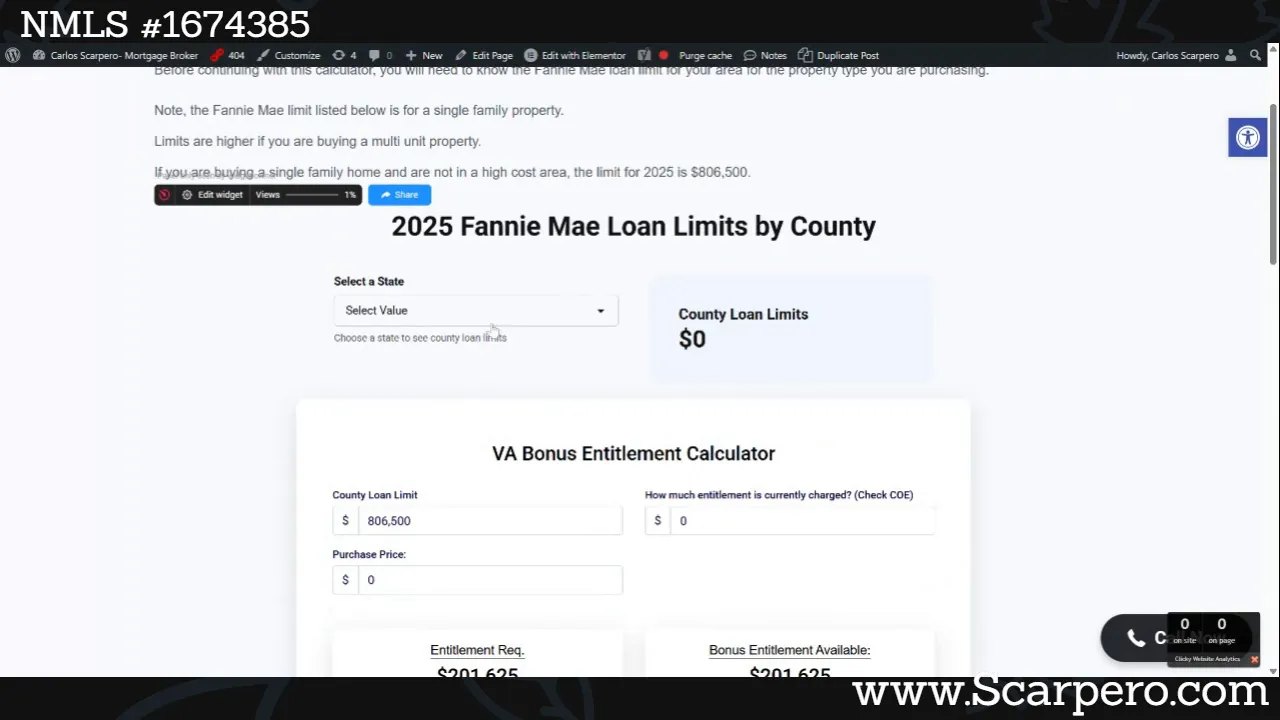

Now, let’s get to the fun part — using the calculator. You can find my free online VA bonus entitlement calculator at scarpero.com/va-bonus-entitlement-calculator. It’s designed to make this process super easy, even if you’re not a mortgage pro.

Here’s a quick walkthrough of how to use it:

- Enter the VA loan limit for your area: This is based on the Fannie Mae loan limits for your county. For example, in Ohio (where I am), the base limit as of 2025 is $806,500.

- Input your current entitlement charge: This is the number from your COE (like the $88,412 in the example).

- Enter the purchase price of the new home: This helps the calculator figure out if you’ll need a down payment.

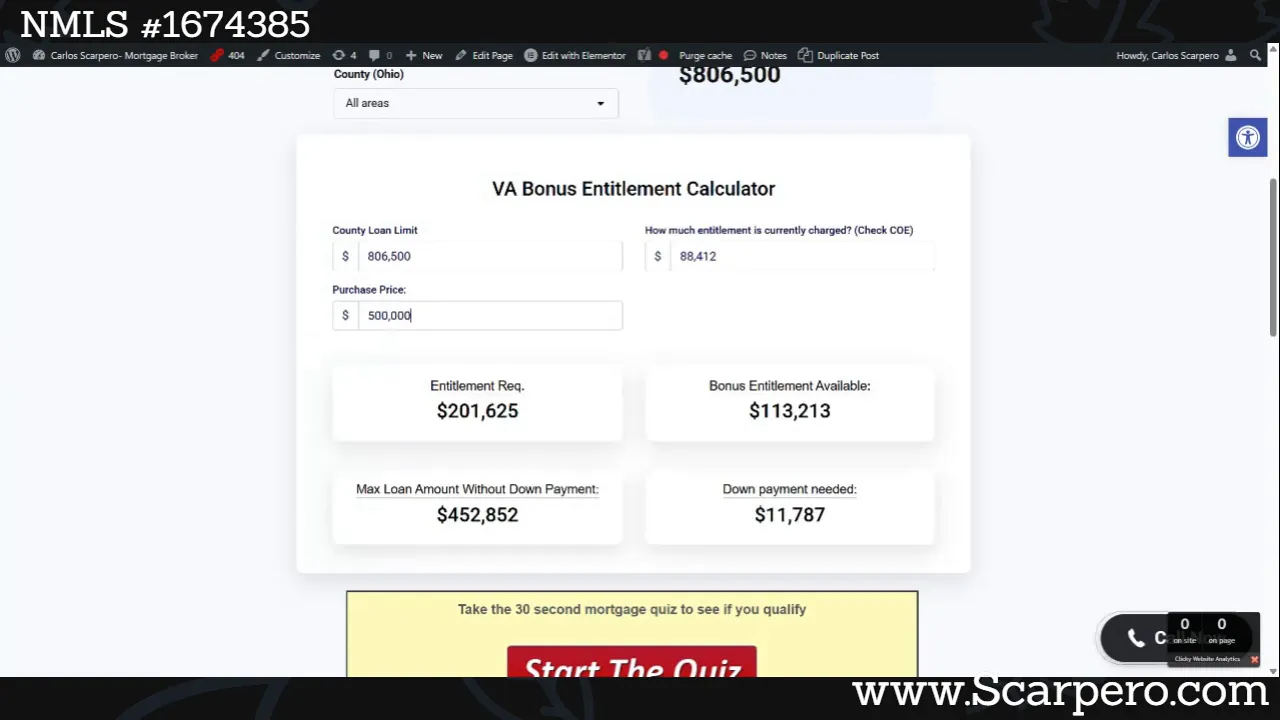

Once you enter these details, the calculator tells you how much you can borrow with zero down based on your remaining entitlement. In the example, with an $88,412 entitlement charge and an $806,500 loan limit, you could buy up to around $452,852 with zero down.

What Happens if You Want to Buy a Home Above That Limit?

Good question! Let’s say you want to buy a home priced at $500,000. The calculator will show you how much down payment you’d need to cover the difference due to limited entitlement. In this case, it’s approximately $11,787.

Remember, while you still need to qualify for both loans financially, this entitlement calculation tells you if a down payment is required. It’s a critical step in your home buying process when using VA benefits multiple times.

Important Details to Keep in Mind

- Loan Limits Vary by County and Property Type: The $806,500 limit is a base number for Ohio single-family homes. If you’re buying a duplex, triplex, or fourplex, the limits will be different and generally higher. You’ll want to look up the specific Fannie Mae limits for those property types in your county.

- Minimum Loan Size: The VA requires a minimum loan size of $144,000 for entitlement to apply.

- Always Bookmark the Calculator: Since you might be looking at multiple properties or revisiting your entitlement status, keep the calculator handy for quick checks.

Why Use an Online Calculator? Because It’s Easy and Accurate!

Even seasoned mortgage professionals can get tangled up trying to do these calculations by hand. The VA bonus entitlement rules and loan limits can be confusing, and mistakes can cost you money or cause delays in your approval.

That’s why I built this calculator—to help you quickly and accurately determine your remaining entitlement and understand your buying power. No more guesswork, no more multiple phone calls trying to get the numbers right.

FAQs About VA Bonus Entitlement and the Calculator

Q: What is VA bonus entitlement exactly?

A: Bonus entitlement is the additional VA loan benefit you get when you already have an active VA loan. It allows you to use your VA home loan benefits again without having to pay a down payment, up to certain loan limits.

Q: Do I always need a down payment if I have multiple VA loans?

A: Not necessarily. It depends on your remaining entitlement and the loan limits in your area. If your entitlement is maxed out, you may need a down payment. The calculator helps you figure this out.

Q: What if I’m buying a multi-unit property like a duplex or fourplex?

A: Multi-unit properties have different loan limits than single-family homes. You need to check the Fannie Mae limits for your county and property type and enter those into the calculator for an accurate result.

Q: How do I find my Certificate of Eligibility?

A: You can request your COE through the VA’s eBenefits website or ask your lender to help you obtain it. It shows your entitlement usage and is necessary for calculating your bonus entitlement.

Q: Can I use the calculator for any state?

A: Yes! You just need to know the correct loan limits for the county and state where you’re buying the property. You can find these limits on the Fannie Mae website or your lender can provide them.

Final Thoughts

Understanding your VA bonus entitlement is key to maximizing your VA home loan benefits, especially if you’re managing multiple loans. Using my free online VA bonus entitlement calculator takes the confusion out of the process and helps you plan your next home purchase with confidence.

If you have any questions or want to talk through your specific situation, don’t hesitate to reach out to me directly at (937) 572-3713. I’m here to help you make the most of your VA benefits and get you into the home you deserve.

Remember to bookmark the calculator page and keep it handy as you look at different homes—it’ll save you time and headaches!

Home Buying

Can You Have Multiple Properties With A Single VA Loan?

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

Credit Tips

How To Get A VA Loan When You Work On Commission

How To Get A VA Loan When You Work On Commission If you earn commission instead of a steady salary, qualifying for a VA loan