Home Buying

Can You Have Multiple Properties With A Single VA Loan?

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

Carlos Scarpero- Mortgage Broker

Take the 30 second mortgage quiz to see if you qualify |

|

|

| Start The Quiz |

When you’re applying for a VA home loan, understanding how your debts are evaluated can make a significant difference in your loan approval chances. One common question I get is whether you can exclude debts that someone else is paying—like a parent, spouse, or child—from your VA loan debt-to-income ratio. The good news is, under certain circumstances, you can. But it depends on the type of liability you have and the documentation you can provide.

In this article, I’ll walk you through the ins and outs of how VA loan underwriting treats debts paid by others, focusing on the critical distinction between contingent and non-contingent liabilities, what the VA guidelines say, and practical steps you can take to work this to your advantage.

The first step is to understand the difference between contingent and non-contingent liabilities because the VA loan rules treat them differently.

A contingent liability occurs when you are a co-applicant or co-signer on a loan with someone else. For example, imagine your child is 18 years old and wants to buy a car, but they don’t have enough credit to qualify for a loan on their own. You agree to co-sign the loan to help them get approved. In this case, the loan is a contingent liability for you because you’re responsible if the primary borrower (your child) defaults, but the payments are expected to be made by the child.

In VA loan terms, if you can provide evidence that the other party (your child, spouse, or whoever) is making the payments reliably, this debt might be excluded from your debt-to-income ratio. This is important because excluding such debts can improve your qualification for a VA loan.

On the other hand, a non-contingent liability is a loan that you took out solely in your name, even if someone else is making the payments. For instance, if you took out a car loan for your 16-year-old child who isn’t old enough to qualify for a loan, you are the sole borrower. If the child pays you back or pays the loan directly, it doesn’t change the fact that you are responsible for the loan. This is a non-contingent liability.

When it comes to VA loans, non-contingent liabilities generally count against your debt-to-income ratio regardless of who is making the payments because you are legally responsible for the debt.

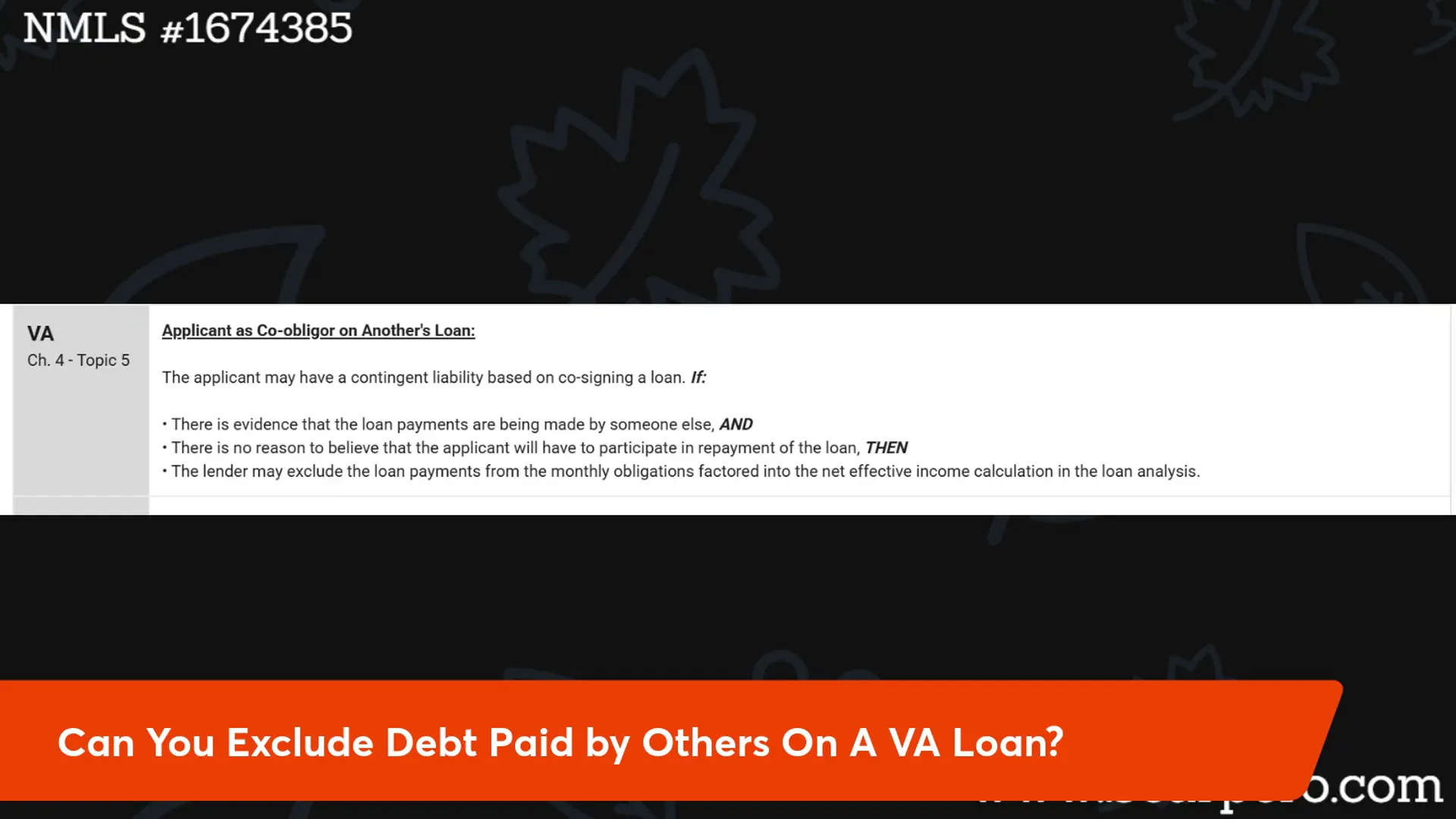

The VA handbook provides some guidance on this topic in Chapter 4, Topic 5, which talks about applicants as co-obligors or co-borrowers on loans. Here’s the key excerpt:

The applicant may have a contingent liability based on cosigning a loan. If there’s evidence that the loan payments are being made by someone else, and there is no reason to believe that the applicant will have to participate in repayment of the loan, then the lender may exclude the loan payments from the monthly obligations.

Simply put, if you are a co-signer and can prove the other party is making the payments, the lender can leave that loan off your monthly debt obligations when calculating your debt-to-income ratio.

However, the VA handbook is somewhat vague on specifics, which is why lenders often have their own interpretations and documentation requirements.

One of the most important things lenders look for when deciding whether to exclude a contingent liability is proof of consistent payments made by the other party. The standard is usually 12 canceled checks or equivalent proof showing the other person has been making the payments on time for at least a year.

This documentation is critical because it demonstrates a payment history and suggests that the other party will continue to make the payments, which reduces your risk as the co-signer.

This rule applies in many real-world situations, including divorces where one party remains on a loan but no longer makes payments. If you can show the other party has been paying for 12 months, the lender may exclude that debt from your obligations.

Late payments can complicate matters. The VA guidelines don’t provide clear-cut rules about how to treat late payments on contingent liabilities, leaving it to the lender’s discretion.

For example, if your child, for whom you co-signed a loan, recently lost their job and missed payments, this could negatively impact your credit—even though you didn’t make the payments late yourself. Some lenders may decide that’s a risk you have to bear, meaning they will count the late payments against your qualifications. Others might exclude the loan from your obligations if they believe the late payments were an isolated incident and the loan is otherwise in good standing.

Take the 30 second mortgage quiz to see if you qualify |

|

|

| Start The Quiz |

Because of this variability, it’s essential to work closely with your lender and provide as much documentation as possible to explain the situation.

Non-contingent liabilities, where you are the sole borrower, are treated differently. It doesn’t matter if someone else is paying the loan; the debt counts against you because you are legally responsible for it.

Here’s a real-life example: A veteran borrower went overseas and gave their car to someone else, asking that person to take over the payments. The new “borrower” failed to make payments, and the car was repossessed. Even though the veteran no longer used the car, the loan remained in their name because they never refinanced or removed themselves from the loan.

Since the loan was non-contingent, the repossession and missed payments damaged the veteran’s credit, and the lender counted the debt against them. As a result, the veteran was denied VA loan approval.

Take the 30 second mortgage quiz to see if you qualify |

|

|

| Start The Quiz |

Yes, if the loan is a contingent liability where you co-signed with your spouse, and you can provide evidence (such as 12 months of canceled checks) that your spouse is making the payments, the lender may exclude that debt from your debt-to-income ratio.

If you are the sole borrower (non-contingent liability), the debt will count against you regardless of who is making the payments because you are legally responsible for repaying it.

While the VA guidelines are somewhat vague, most lenders require proof of 12 consecutive monthly payments made by the other party to exclude the debt. This is a common industry standard to demonstrate consistent payment history.

Late payments complicate the situation. The VA allows lenders to use their judgment. Some lenders will count the late payments against you, while others may exclude the debt if they believe the late payments were isolated and the loan is otherwise current.

Yes, if possible, refinancing or otherwise removing your name from the loan can help. This is especially important for non-contingent liabilities where you are the sole borrower.

Applying for a VA loan can be complex, especially when you have debts that someone else is paying. The key to navigating this successfully is understanding the difference between contingent and non-contingent liabilities and being prepared to provide thorough documentation to your lender.

Always communicate openly with your lender, as each situation can be unique and lenders may have different interpretations of VA guidelines. If you’re unsure how your debts will be treated, don’t hesitate to ask for personalized advice to help you position yourself for approval.

If you have any questions about VA loans or need help with your specific situation, feel free to reach out. I’m here to help you understand the process and work toward your homeownership goals.

Good luck with your VA loan journey!

Contact Info: You can reach me at (907) 572-3713 or visit scarpero.com for more information and personalized assistance.

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

How To Get A VA Loan When You Work On Commission If you earn commission instead of a steady salary, qualifying for a VA loan

Can You Refi a VA Loan With Bad Credit? If you have a VA loan and a low credit score, you might assume refinancing is