Home Buying

Can You Have Multiple Properties With A Single VA Loan?

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

Carlos Scarpero- Mortgage Broker

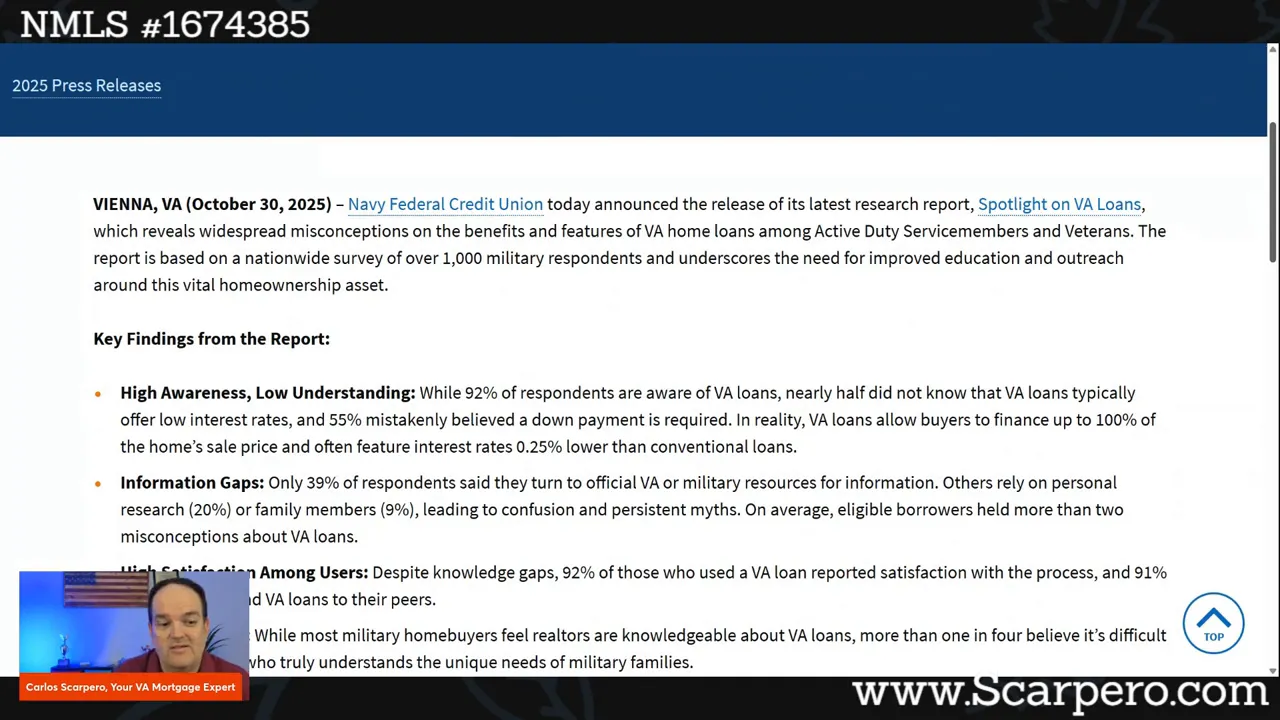

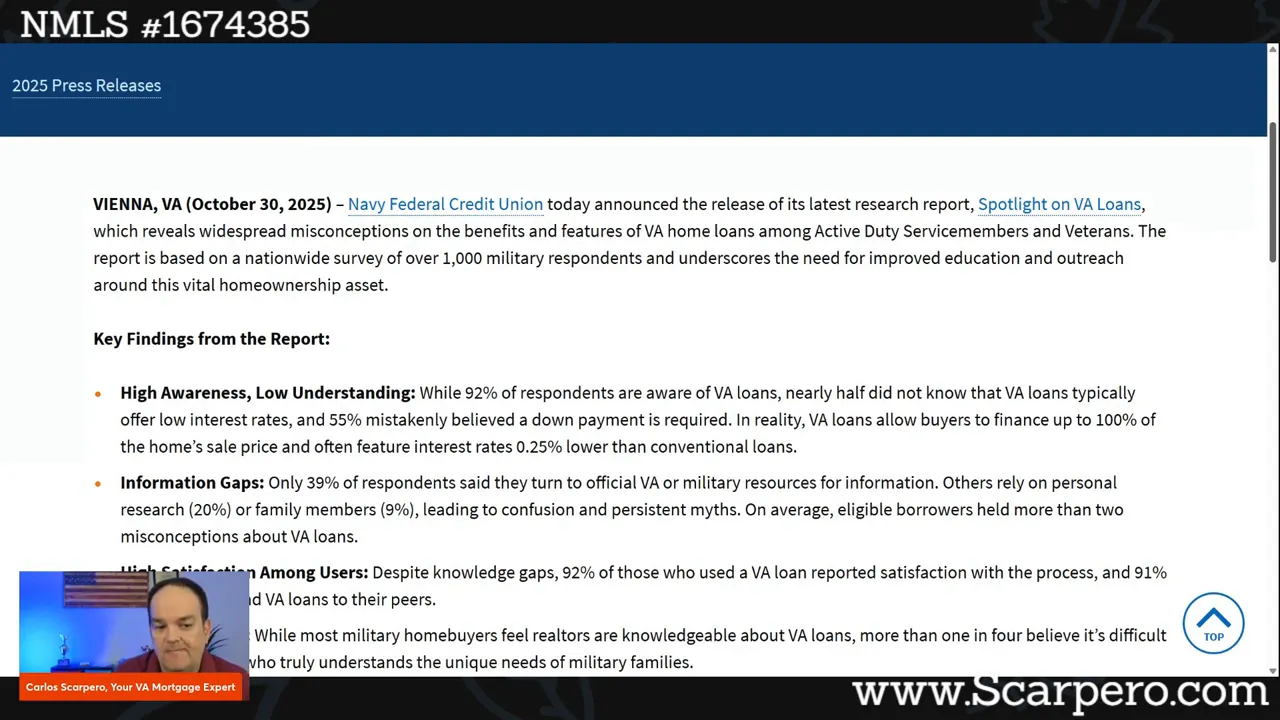

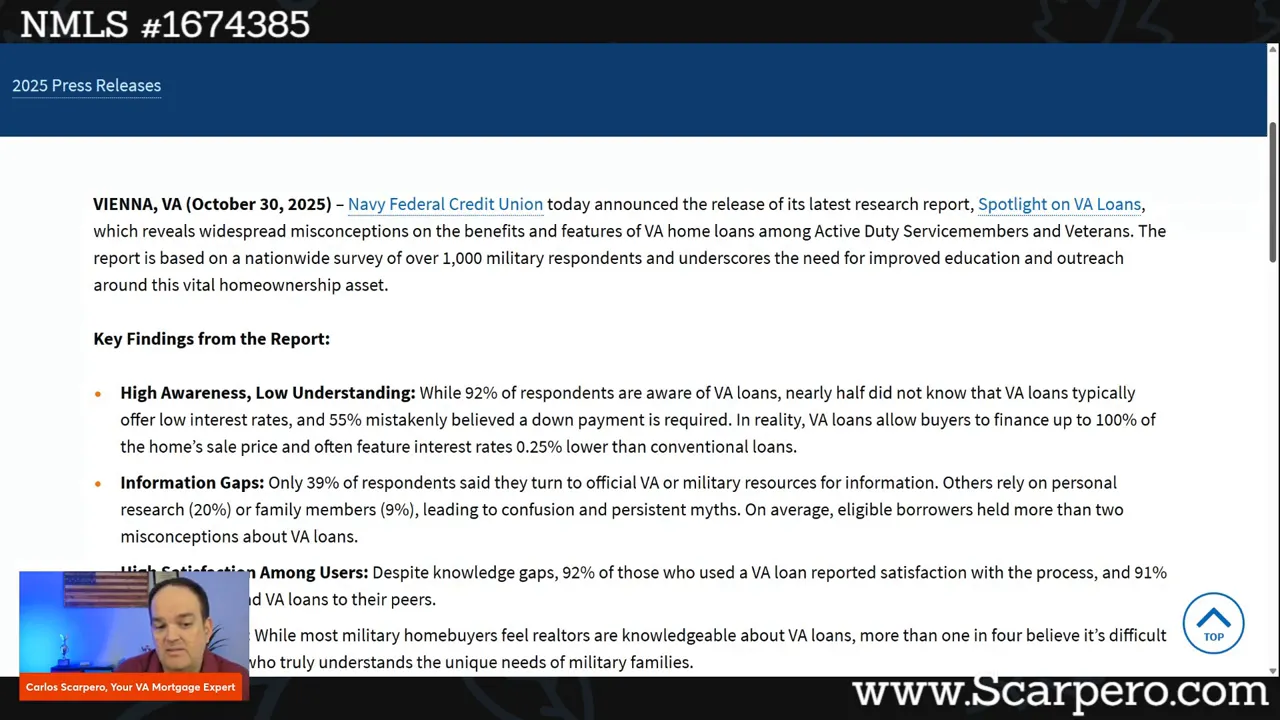

You probably know VA loans exist, but you may not realize how many eligible service members and veterans still misunderstand what they offer. A recent survey from Navy Federal Credit Union exposed a surprising gap: awareness is high, understanding is not. That gap creates myths, missed opportunities, and unnecessary confusion at the exact moment people need clarity most—when they are buying a home.

The survey reveals four headline findings that matter if you are thinking about using VA benefits for homeownership:

Awareness alone isn't enough. You can know a program exists and still miss the benefits because of outdated or incorrect beliefs. Two of the most damaging misperceptions in the survey were that VA loans require a down payment and that they do not offer competitive interest rates.

The survey highlights a big reason for these misperceptions: people are not consistently turning to official or expert resources. When only 39% of respondents consult the VA or military resources, the other 61% rely on hearsay, outdated internet posts, or friends. That is how myths persist.

Eligible borrowers in the survey held, on average, more than two misperceptions about VA loans. That is not just a few misunderstandings — it is multiple barriers to making an informed decision.

Despite the knowledge gaps, people who used a VA loan reported high satisfaction. Roughly 92% said they were satisfied with the process, and 91% would recommend a VA loan to peers. That tells you two things: the product works for those who use it, and the problem is primarily informational, not performance.

Finding a realtor who truly understands military life and VA-specific contract language can be challenging. The survey found more than one in four respondents believed it was hard to find a realtor who grasps military-unique needs. That matters because a realtor who knows VA rules can:

If you are eligible for a VA loan or helping someone who is, here are concrete steps to close the knowledge gap and avoid avoidable mistakes:

Loan officers and realtors are on the front line of correcting misperceptions. Producing plain-language content, answering common questions proactively, and offering referrals to trusted, experienced partners will shorten the learning curve for eligible buyers.

If you are a loan officer, consider making short, focused posts that tackle one myth at a time. If you are a realtor, highlight your VA experience in listings and client conversations. Small, practical actions multiply across networks and reduce the number of people who rely on inaccurate information.

Take the 30 second mortgage quiz to see if you qualify |

| Start The Quiz |

The key point is straightforward: VA loans work well for many eligible borrowers, but knowledge gaps keep people from taking advantage of them. Awareness without understanding is not helpful. Closing that gap takes reliable information, experienced professionals, and a willingness to correct myths when you see them.

If you need help finding a knowledgeable realtor or want a clear answer about VA loan options, reach out to a trusted mortgage professional in your area. Strong guidance will help you use the benefit you earned with confidence.

No. In most cases, eligible borrowers can finance up to 100% of the home sale price with a VA loan, which means no down payment is required. Exceptions exist, such as when the purchase price exceeds your entitlement or seller concessions are limited, so discuss specifics with your lender.

Yes. VA loan rates are typically lower than conventional loan rates. The exact difference varies with market conditions, but many veterans and active duty buyers see a meaningful rate advantage that lowers their monthly payment and total interest paid.

Start with official sources like VA.gov and reputable lenders or credit unions that specialize in VA lending. Also ask for referrals to realtors and loan officers who regularly handle VA transactions.

Ask agents about their VA transaction experience, request references from military clients, and verify they understand VA contract provisions. A good realtor will explain how VA requirements affect inspections, repairs, and closing timelines.

Reach out to a local VA-experienced lender or realtor. If you don’t have one, ask around in your network or contact an established mortgage professional who can make introductions.

Knowledge changes outcomes. The better informed you are, the more likely you are to use benefits wisely and secure a home that fits your needs.

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

How To Get A VA Loan When You Work On Commission If you earn commission instead of a steady salary, qualifying for a VA loan

Can You Refi a VA Loan With Bad Credit? If you have a VA loan and a low credit score, you might assume refinancing is