Home Buying

Can You Have Multiple Properties With A Single VA Loan?

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

Carlos Scarpero- Mortgage Broker

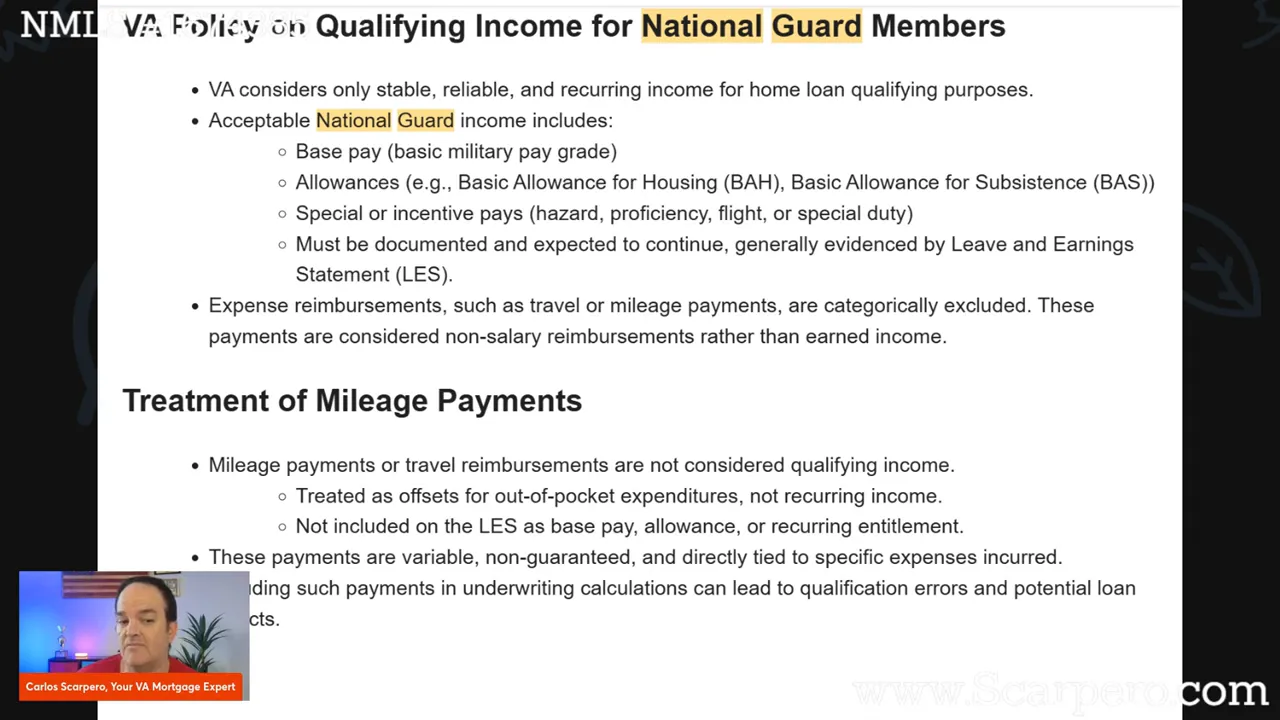

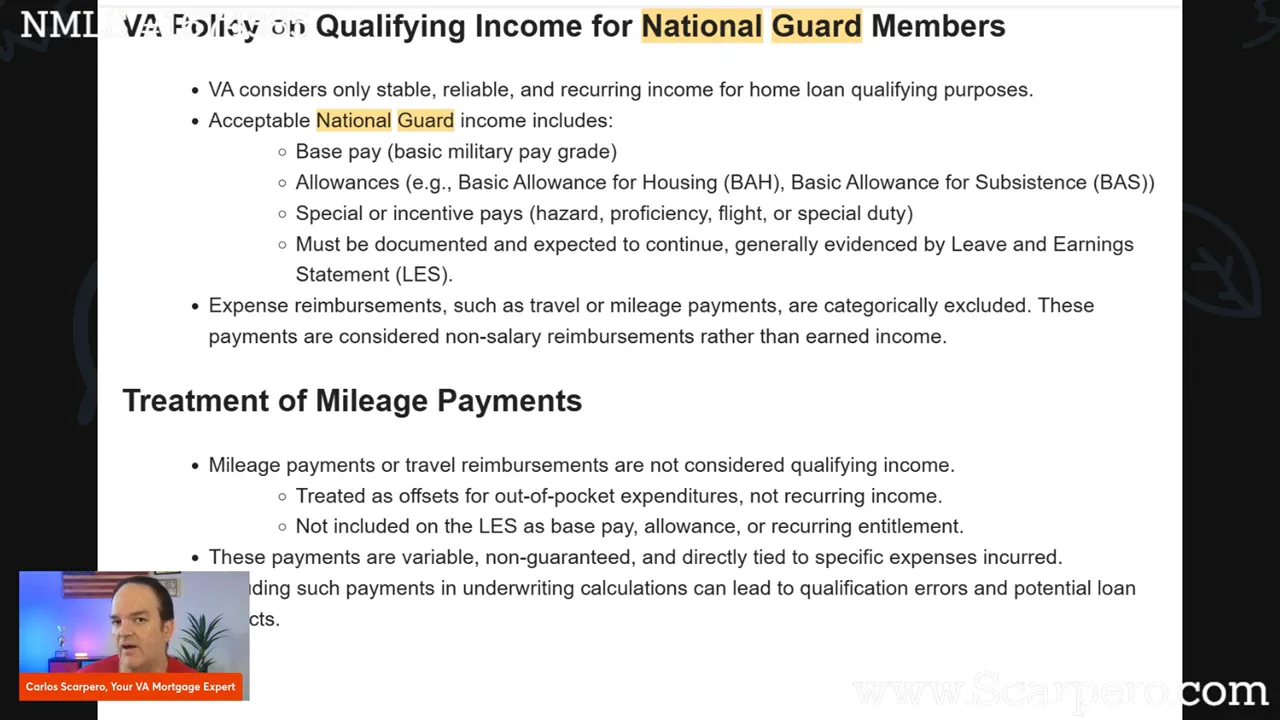

If you serve in the National Guard and receive mileage reimbursements or a mileage bonus because your duty station is far from home, you might wonder whether that money can help you qualify for a VA home loan. The short answer is no. VA underwriting rules exclude mileage and travel reimbursements from qualifying income because they are reimbursements for expenses, not stable, recurring pay.

The VA’s underwriting guidance makes a clear distinction between true income and expense reimbursements. The handbook states that qualifying income must be stable, reliable, and recurring and must be documented and expected to continue. Expense reimbursements are categorically excluded.

"Treatment of mileage payments or travel reimbursements are not considered qualifying income. These reimbursements are offset for out-of-pocket expenses, not recurring income. It is not included on the LES as base pay or an allowance."

Mileage pay is intended to cover the cost of driving to and from duty. It compensates for fuel, wear and tear, and other out-of-pocket expenses. Because the payment’s purpose is expense reimbursement, underwriters do not treat it the same as base pay, allowances, or special pay that represent earned income.

Qualifying income needs to be predictable and expected to continue. Mileage reimbursements often vary month to month depending on your schedule, orders, and travel needs. That variability, combined with the reimbursement nature, is the key reason it does not count toward your debt-to-income calculation.

While mileage does not qualify, the VA does accept other types of military-related income when they meet the stability and documentation tests. Examples include:

For any income to count you will need proper documentation and evidence that it is likely to continue. Typical documentation includes LES (Leave and Earnings Statement), award letters, employment verification, or tax returns.

If you depend on a mileage bonus as part of your monthly budget, you should plan for it not being counted by VA underwriters. That doesn’t mean you can’t get the loan—just that qualifying income will be based on other pay items that meet VA criteria.

Common scenarios and practical implications:

Use these steps to make the underwriting process smoother and maximize the income that will count:

If mileage reimbursements are an important part of your household budget, consider these options:

Generally no. The VA guidance states mileage and travel reimbursements are excluded because they reimburse out-of-pocket expenses rather than represent recurring income. If a payment is coded on the LES as a recurring allowance or special pay that the VA recognizes as income, underwriters may consider it. Always confirm with your lender and provide the LES and any award letters for review.

Take the 30 second mortgage quiz to see if you qualify |

| Start The Quiz |

Even if it is consistent, mileage is still classified as an expense reimbursement and typically will not be counted. The determining factor is the nature of the payment, not just its regularity.

Yes. Drill pay or reserve pay can be counted if you can show a history and documentation indicating it is likely to continue. Two years of stable history or a clear pattern documented on pay records or tax returns strengthens the case.

Bring LES statements, pay stubs, W-2s or tax returns, orders or award letters, and any documentation that shows recurring special pay. If you receive mileage payments, keep them for your records but be prepared that underwriters will likely exclude them.

Mileage and travel reimbursements from the National Guard do not count as qualifying income for VA loans because they are reimbursements for expenses and are not treated as base pay or recurring allowances. Focus your application on income streams the VA recognizes: base pay, allowances, special pay that is documented and expected to continue, and stable civilian income.

Being prepared with the right documentation and understanding how the VA defines qualifying income will help you avoid surprises during underwriting and position you to get the best possible outcome for your loan application.

If you received mileage reimbursements and are preparing a VA loan application, use this quick checklist to make sure your application focuses on qualifying income the VA will accept.

Suggested questions to ask your lender before applying:

If you need more help, consider contacting a VA-savvy lender or housing counselor who can review your LES and pay documents and advise on documentation strategies tailored to National Guard pay scenarios.

Can You Have Multiple Properties With A Single VA Loan? You’re trying to buy a property and it includes more than one parcel or lot

How To Get A VA Loan When You Work On Commission If you earn commission instead of a steady salary, qualifying for a VA loan

Can You Refi a VA Loan With Bad Credit? If you have a VA loan and a low credit score, you might assume refinancing is